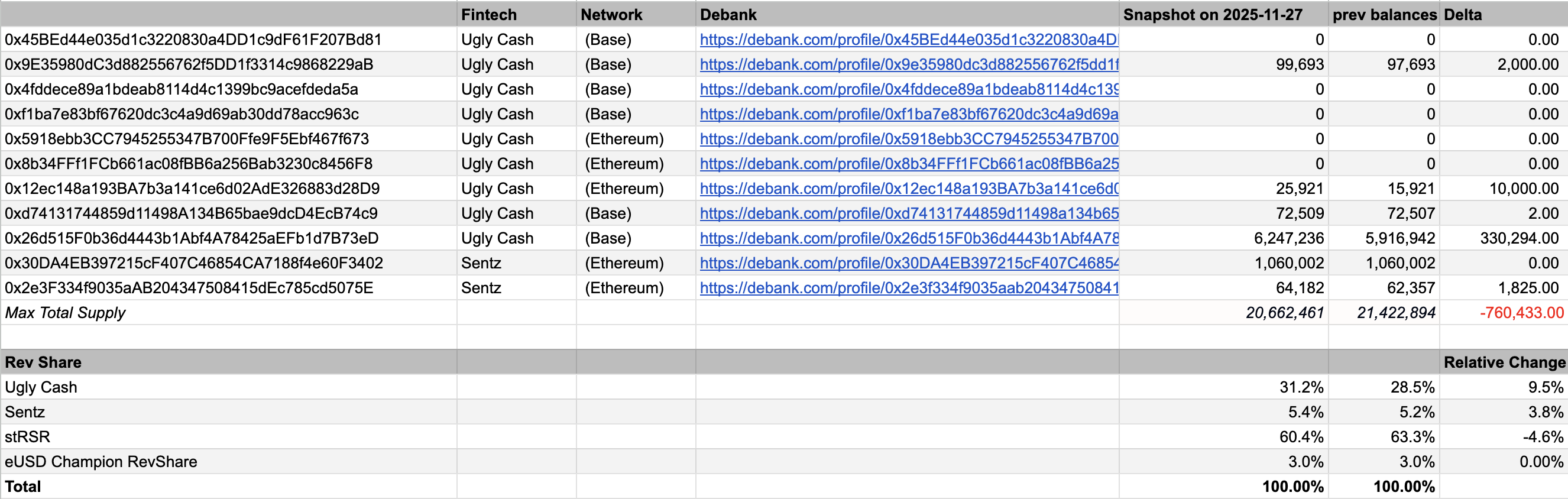

This is an update to the existing ongoing proposal of sharing some of the eUSD Revenue with FinTechs(Ugly Cash and Sentz). eUSD shares underlying revenue with distribution partners(i.e. fintech apps) who use and promote eUSD for their customers.

Would help if you mentioned how this affects RSR stakers. I’ve been seeing the percentage drop every other week but no explanation how this affects anyone at all. Please be transparent, is this good for the ecosystem? Does this benefit RSR stakers?

Hi, please familiarize yourself with the original proposal here

Personal opinions shouldn’t be discussed in the update proposals. It’s important to only present the facts to the governors.

My personal opinion is that eUSD’s only distribution is through the FinTechs, and that supporting the FinTech RevShare proposals is the only way that eUSD will find PMF.

The overcollateralization percentage is dictated by the following factors: Collateral basket APY, amount of RSR staked, the price of RSR and revenue percent directed towards stRSR. In recent events the revenue percent directed towards stRSR has been going down. However, during this time period the APY to stake your RSR has been going up.

Hey glock, you should definitely check out the original proposal as Sawyer suggests. I’d also suggest checking out the latest quarterly report and this forum post to really get up to speed on eUSD and sentiment around the revenue share programme.

I agree with Sawyer on eUSD’s main distribution channel being through fintechs. However to answer your question candidly, while it’s easy to derive from the proposal that supporting these early fintechs and their growth will eventually benefit RSR stakers, there is currently no clear plan for a revenue share to return to them.