First of big shout out to @Sawyer for meticulously documenting these changes every other week and grinding the governance work.

We want to present a historical view of the eUSD revenue share development and also summarize pertinent questions that come up time and again in the weekly DTF governance standups.

First off: How did the eUSD revenue share progress over time?

We can see that UglyCash is really growing their eUSD balances, and seems to be buying eUSD on the open market vs minting new eUSD.

All in all the revenue share is definitely helping them grow, it seems.

So far, no further insights into the use of funds or user growth have been forthcoming from their team.

eUSD stakers have repeatedly called out a desire for more information on how the rev share is used by Sentz and UglyCash, and to see more detailed progress reports form their teams.

IPs with revenue share updates pass regularly, even in the absence of said information.

Other eUSD governors have called out that the experiment is not time boxed, and not end date is set. While this is formally true, eUSD governors can put an end to the experiment every two weeks by voting against the latest revShare update, and/or by submitting a formal proposal to end it.

TL;DR: The experiment seems to be very successful, eUSD governors seem to be happy to continue the revenue share, more information from UglyCash and Sentz would be welcome.

Thanks for putting this together Raph, great to have an overview of how the rev share has progressed without having to go into each proposal individually.

My only gripe with the data presented is that we can’t definitely say that fintech held eUSD is growing in dollar terms because only percentage change has been presented, displaying fintech relative to non-fintech change. I think the addition of a dollar terms analysis would complete this data set and a stacked bar chart could combine all data points nicely.

Could also be something else to include in the Quarterly reports @Sawyer?

eUSD rev share participation is materially outpacing its TVL, and lagging overall stablecoin category growth. Also eUSD’s stRSR incentives for security are dropping.

Observation:

eUSD made 17 rev share adjustments in 12 months. High-frequency changes with no clear material impact. This cadence risks governor fatigue and lacks alignment with rev share participant transparency on fund usage and impacts—missing chances to build shared ownership and compounding community trust. It reads more like busy work than strategic adaptation.

Recommendation:

Shift eUSD to quarterly rev share adjustments to reduce governance load and improve quality/depth of updates. Require each revenue participant to post a data-backed update in the RFC for review by the community and governors before they vote to adjust rev share %. Like any role, compensation for each of Sentz, Ugly Cash and eUSD Champion should follow clear, demonstrable outcomes, not assumptions or inertia.

Here is the associated data table for the above charts and findings: (TVL data from CoinGecko)

I plan to vote AGAINST all future eUSD revenue share change proposals unless recipients each individually (Sentz, Ugly Cash, RToken Champion) provide written updates posted to the relevant RFC, before the onchain proposal vote. These updates may include past/future specific goals, use of funds to grow their respective (our shared) ecosystem, whats working, whats not working, and any other relevant learnings. This is table stakes in modern day decentralized ecosystem governance.

I encourage fellow eUSD governors to do the same.

Being part of a shared ecosystem includes steady 2-way dialogue on contributions. If you’re being compensated, it’s reasonable to take the lead sharing the outcomes and learnings.

If we’re fielding 24 revenue share proposals a year, we should see 24 meaningful updates from each rev share recipient in return.

Regarding frequency…

Startups are hard. Every administrative distraction risks diluting more growthy efforts. At present, this 24x per year rapid-fire run rate feels mismatched to the reality of results. A quarterly rhythm—four proposals, four in-depth updates—would support deeper reflection and engagement.

If eUSD’s TVL starts outpacing the broader stablecoin market (per DeFiLlama), a faster cadence could be justified.

The only current distribution that eUSD has available to it is the Fintech Revenue Share program. The amount of eUSD held by fintechs is growing at a rapid pace, 4-8% week over week. With this in mind I think governors should strive to align themselves as closely as possible with the fintechs to continue to support their growth and use of eUSD.

The FinTechs use the revenue they earn from eUSD to pass along to their users of their apps in their respective earn programs. Seeing the customer assets under custody rate increase or the individual FinTech wallet balances increase is an indication that there are more users being onboarded and more users are depositing their funds into these programs.

With regard to the recommendation of frequency of the bi-weekly update proposals, your suggestion of moving them to quarterly will cost the FinTechs significant Revenue. If we use Ugly Cash as an example, if we look back at the revenue earned in Q2 with bi-weekly rebalances we have a current distribution of $24,176. If the frequency of these proposals were to drop to quarterly we’d see their revenue for this period drop to ~$13,538. If governors decided to move to monthly, we would again see the FinTech’s lose out on some of their revenue. The FinTech’s don’t have to use eUSD as the asset or yield vehicle of choice. They can easily use sUSDS or another yield bearing asset. Or they can move offchain to T-bills where they will receive 100% of the yield on their users deposits. They use eUSD for the support they get from the governors and to align themselves with the Reserve Ecosystem.

Having the FinTechs share in-depth statistics of their app and user base is fairly complicated. Ugly Cash and Sentz are competitors and they would not want their competitor to see any internal data of what is working and what is not. Because of this, it puts me in a very peculiar spot, as I have communication with FinTechs and I understand them not wanting to share too much information. But on the other hand, it is very important to be as transparent as possible.

After writing this response I think another data point I can include in the quarterly reports can be FinTech income earned from the eUSD RevShare. In the bi-weekly updates I include the data that we see with the changes in wallet balances in eUSD from proposal to proposal. As far as my personal earnings are concerned. I do not use the RToken revenue to pay for my RToken expenses(or personal expenses). I cover those out of my own pocket. When I start paying any expenses with the Revenue that I earn from the RevShare I will happily post about it on the forums. Here is a video covering some of the expenses I incur.

Lastly, James, you are a valuable member of the Reserve Ecosystem. For those that don’t know, James was a seed investor in the Reserve project alongside Peter Thiel and Sam Altman, James was the Head of Ecosystem at ABC Labs and played a key role in growing the project’s TVL from 0 to $250M+. James, I would appreciate your support and understanding of why these need to be bi-weekly, additionally I hope you know that I am relentlessly trying to improve the transparency of the FinTechs. As always, I appreciate your feedback and you are being heard.

I can see @0xJMG point on vote fatigue.

Seems to be an unfortunate scenario of the current capabilities of the Reserve Protocol here.

This isn’t a new proposal vote, it’s a ratification vote.

These votes don’t signal a change in terms or structure. We’re simply confirming numbers for what was already agreed to: growing eUSD usage through high-yield incentives. If anything, this cadence exists because the program is working.

Would much rather the protocol was automated here and we can be voting on strategic implementation shifts of the program, but oh well, for now.

I also agree with @0xJMG point that startups are hard and administrative distraction risks diluting growth efforts. He’s savvy & experienced.

And that’s what we want to stay doing.

It’d be important to balance what information is useful to help governors make decisions & fintech partners efforts + unique insights advantage.

It’s already great information about our growth rate overall from the rev share proposals without giving away key strategic insights that help competitors who scour the interwebs.

We have a strong communication on social channels that can be referenced for public initiatives b/c of our build in public mentality. I wouldn’t be surprised if peeking that monthly + the tangible eUSD growth results would satisfy that we are demonstrating outcomes (and the outputs of how are visible).

I see stablecoin Yield to consumers as table stakes.

It’s rapidly becoming non-negotiable to get treasury APY or DeFi APY as a stablecoin holder. That’s not what we really should be spending our energy on together.

But there are unique advantages for eUSD that we promote.

There are bigger questions coming as we achieve more success. Like…as we scale to $50MM, $100MM and beyond…what’s the right amount of safety net for our customers, what they value and will “pay” for vs. the risk of RSR stakers.

Those will be coming, but let’s take @0xJMG advice and not spend too much time on initiatives that prevent focus on growth for us to get there.

One thing to note here is that voting NO on these proposals doesn’t stop the revenue share, just keeps the ratios unchanged.

So if the goal is to get fewer $$$ to FinTechs then voting FOR on any lower proposals and NO on others or suggesting a stop to the revshare or an amendment to the frequency via a standalone proposal would be the way.

All of these actions are legitimate governance activities. Just pointing out the differences in consequence.

I appreciate the healthy discussion on this forum post and the conversation we had on the latest GovOps concerning eUSD, found here. Both have been extremely helpful in formulating my own opinions on the path forward for eUSD.

Firstly, i’d like to share some of the eUSD data i’ve worked on since the creation of this forum post. Given that these are some of the most pertinent data points for eUSD right now I wanted to make them as easily digestible as possible, reducing friction for other governors who don’t have the time to look into the data themselves.

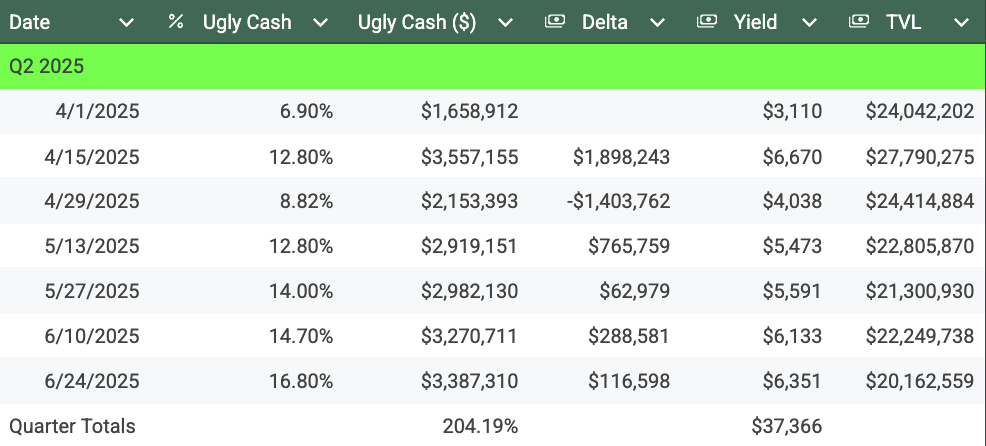

Figure 1 - Historical Revenue Share and Over-Collateralisation

This chart presents the varying revenue distributions at each snapshot since the start of the revenue share programme and has the over-collateralisation, OC super-imposed. As we can see fintech holdings and rev share has grown while eUSD TVL has remained relatively flat, which strongly suggests fintechs are swapping into eUSD rather than minting, a trend I think we will see reverse if fintechs continue along the same growth trajectory we have seen up until now. Naturally, over the same duration we have seen the OC drop from 111% to 71% as revenue share is taken away from Staked RSR holders and given to the fintechs, a trend I think will continue as long as we see sustained fintech growth.

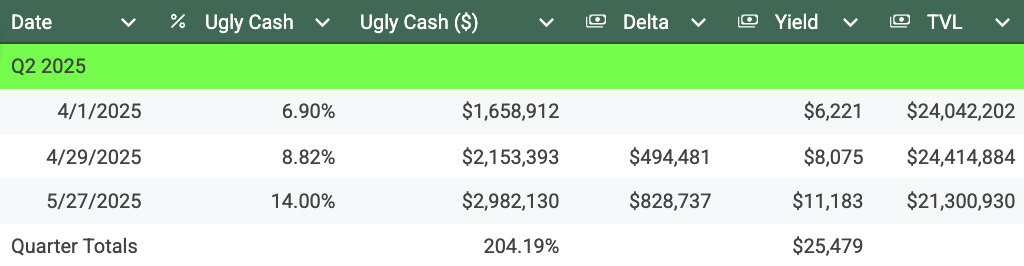

How the frequency of rebalances affects revenue distributions

This work came off the back of @0xJMG comments about RFC frequency and governor fatigue. The data here is rough and ready using what was available from @Raphael_Anode and @0xJMG tables, I didn’t have time to snoop on the chain myself and pin these exactly, E.G in Figure 2 the final data point - 6/24/25 spans two quarters falsely inflating the Figure 2 totals. I think it’s accurate enough for our needs showing the amount of revenue that would be distributed to Ugly Cash, UC at various RFC frequencies.

TLDR - Given UC’s sustained growth every quarter at least bi-weekly rebalances are required to match their holdings and most optimally supports their Earn programme.

All of the data can be found here and if anyone finds holes in it I’m more than open to discuss it further. I also strongly encourage @Sawyer to take over the torch here and continue to collect future data and display these in upcoming quarterly reports to demonstrate to governors why this programme should continue and why we must persist with bi-weekly rebalances for the time being. If you chose to do so please check the eUSD TVL data as @0xJMG said on the latest GovOps that he collected data from Coingecko which may be inaccurate when compared to the Reserve Register.

Path Forward for eUSD

Personally, I agree with @Sawyer that the only avenue for growth available to eUSD is via fintechs and as such I’m a strong supporter of the revenue share programme but I don’t think that the programme and eUSD growth shouldn’t come at the detriment to eUSD stakers as it does in it’s current format.

There are three optimisations that I would like to see occur; increased transparency from fintechs, decreased RFC frequency and a clear understanding of what is an acceptable level of over-collateralisation for the fintechs holding eUSD and a plan of what will happen once we reach it.

Transparency

I think the best argument for increased transparency is the discussion @Raphael_Anode and @Sawyer has in the latest GovOps call so won’t outline it again here but I’m heavily in favour. Just like @josh said in his comments that it’s becoming a non-negotiable that stablecoin holders get treasury APY, it’s also a non-negotiable that incentive programmes require documentation especially since as stakers we’re currently providing OC at no cost on all fintech eUSD holdings.

I agree with Raph that this is table stakes across incentive programmes and I encourage UC to instead of coming to the forums and asking us to check their socials, check the chain for data to come to the forums instead, I suggest updating us on publicly available data once a quarter and feel that a addendum under Sawyer’s quarterly report will satisfy most governors, this satisfies documentation requirements and is also a gesture of good faith, showing us you that you value and respect our commitment to supporting your continued growth and for proving the over-collateralisation which you have said you use in your marketing materials.

I respect your time and commitment to keep key strategic insights secret which is why I suggest completing this once a quarter in line with the quarterly reports and will accept data which is already public knowledge or data that can already be found by your competitors easily.

RFC Frequency

I also think this was covered in detail in our last call and encourage anyone whose got this far down this post to listening to that in full. I hope the data above further supports the ongoing need for bi-weekly ratification votes. However, I’m also deeply concerned about governor fatigue and think we as eUSD governors should work towards governance flow optimisations to reduce the amount of votes required. I look towards people like @Raphael_Anode, @pmckelvy and @mattimost for their input into this and think Tom’s own comments from the original revenue share proposal, found below, and Raph’s around Optimistic Governance are great stepping off points for this discussion.

Over-collateralisation of eUSD

Finally, I’m also concerned about the inverse relationship of fintech revenue share and the levels of OC eUSD enjoys. As expected with growing fintech rev share we’re seeing a decrease in eUSD’s OC ratio. Given this inverse relationship and the expectation that fintech growth will continue I expect eUSD’s OC to continue to drop. While I find that acceptable at current levels given the large degree of OC eUSD currently enjoys, ~80% i’m concerned that with sustained growth and unchecked rebalances the levels of OC will eventually drop below permissible levels.

It looks like this is already being considered by fintechs given @josh remarks.

However, I would rather be proactive rather than reactive with these discussions, avoiding a future where we are making quite decisions in a pinch that leading to bigger issues for eUSD and the protocol further down the road.

Next Steps

As an eUSD governor and delegate I don’t think any of these requests are out of pocket and all would go a long way in furthering the symbiotic relationship eUSD has cultivated with the revenue share programme between fintech and governor.

Given some of these changes require more discussion, governance changes or engineering work I don’t expect them to happen overnight but think they should be worked on by all stakeholders over the coming months.

I feel the end of the quarter is a suitable timeframe for the fintechs to address the issues around transparency and lines up well with Sawyer’s Q3 report and until the end of Q4 for the issues raised around RFC frequency given the strongly likelihood of governance and engineering.

If any of these items aren’t addressed in a timely manner I’d be open to submitting or supporting a RFC to end the revenue share programme, although I hope it doesn’t come to this!

Hey @Sawyer could you drop the simplest version of the eUSD rev share formula here in the RFC, or confirm mine below is correct? Want to be sure I am aligned on what’s in the numerator and denominator so the convo stays precise.

My understanding:

Revenue Share % = (eUSD held by a fintech’s wallets) ÷ (Total eUSD supply)

Writing the concerns/questions in text here for your convenience:

Two week table. This appears to be an apples-to-oranges comparison. Aug in this table but not in the others. Exclude it to maintain consistency (and monthly rev share is better for UC).

Monthly table. Why is June counted in Q3 when it should be in Q2?

Monthly table. Why wouldn’t monthly rev shares be calculated on the last day of the period?

Monthly table. Complete months must be included in the math. For example only a fraction of July is counted.

Quarterly table. Why wouldn’t quarterly rev shares be calculated on the last day of the period?

Quarterly table. Nearly all financial systems (corp reports, taxes, bank statements) anchor to period-end dates for clarity, consistency, and auditability. Mid-period cutoffs invite confusion.

Will address some of the other (good) ideas once we get a little more clear on some of the underlying maths.

Very good discussion going on above. I think a key sticking point that was alluded above for quite a few people, in my viewpoint, is the rather slow TVL growth for EUSD. This is correlated with the increasing Rev Share to Fintechs and the shrinking Rev Share for stRSR holders as @0xJMG mentioned. This means that a lot of the Rev Share growth for the Fin Tech participants are market buys and not mints which I think generates a lot of friction in the community.

As a compromise, would a solution perhaps be that in order to participate in the Rev Share program, that a portion of any new $EUSD funds that are added to Fin Tech wallets be minted instead of market bought?

I do understand that this acts as essentially a ‘tax’ in favor of stRSR holders. For example, let’s say for argument’s sake TVL is $1,000,000. Market buying $100,000 gives you a 10% share vs market buying $75,000 and minting $25,000 which gives you a 9.76% share ($100,000 / $1,025,000).

However, if we want to attract greater attention $EUSD in the long term as a serious contender and maintain strong stRSR participation, I believe growing TVL is essential. Otherwise this just stays a game of who can buy more $EUSD off the open market.

I understand your comments and the answers mostly boil down to limitations in the data set and me being unwilling to put more time into further data collection. In an ideal world we’d have snapshots at the start of every month that easily fit within quarter but without spending time on this and collecting more data we only have the data points on dates that Sawyer snapshotted the wallets in preparation for the next RFC which is where most of the confusion starts, i’ve tried to push the data into the quarters as best I could but there is some overlap e.g Q3 for monthly revenue has 6 extra days which should be allocated to Q2 because of how the RFC schedule fell, the same is true for the bi-weekly rev share which has 6 extra days in Q2 for the same reason.

Still, I’ll comment on all your concerns / questions in order so we can work out the best way to present this data.

Question 1 - It’s best to disregard Q3 when looking at the data tabled in the excel because Q3 hasn’t yet finished, this is why I opted not to include Q3 in the screenshots I posted in the previous comment. I’ll make some changes to the sheet to highlight this further.

Question 2 - June has been pushed into Q3 because of the restrictions with the data set we’re working with. Given the current cadence we’ll miss a few days off the end of the quarter which will be pushed into the Q4 calcs so this will balance itself out a little.

Question 3 - I agree they should but this was impossible with the data I had to hand.

Question 4 - I’d argue that the majority of June is counted in Q2 with only 24th to the 30th being pushed into Q3.

Question 5/6 - Again limitations in the data set. In an ideal world these would be.

TLDR - The data set is extremely week and can be improved significantly with some data collection leg work. I’d take all numbers with a pinch of salt until that work is done but I still think it provides some clarity on the rational behind bi-weekly rebalances.

@ham@Mr_Bones@Sawyer unless I am really missing something I would argue we do not care whether UC and Sentz get their eUSD via Swaps or Mints.

eUSD demand, is demand. This is one of the great benefits of onchain if its in a verifiable wallet.

For example if there is $1M in eUSD demand via Curve pool, this creates an eUSD peg maintennce arb opportunity for traders to mint at lower price $1.00 and sell into the pool at higher price $1.001. I think thats right but hopefully a more attuned trader in the community can verify?

Sure it would be easier for this conversation if they were all mints, but we aim here to make it net-easier-yet-most-effective for all stakeholders to grow, safely.

I could be wrong about some of the above and invite any of the onchain professorial types to critique.

Here is the latest proposal which highlights that number shift in Ugly Cash’s percent.

Moreover I think @Mr_Bones has an excellent take and I tend to agree with him. AFAIK its been cheaper for them to swap on base as opposed to mint on mainnet and then bridge to base. Hence why they have been swapping. However, eventually if Ugly Cash continues to grow at the rate they are, there wont be enough eUSD liquidity on Base and they will be forced to mint on mainnet then bridge to Base. Here is Ugly Cash’s largest wallet(on base): DeBank | Your go-to portfolio tracker for Ethereum and EVM

@Sawyer I would like to see the spreadsheet data and calcs on the quoted math above.

As previously metioned we should be running the math on a sufficiently large dataset of ~6 months of eUSD TVL comparing monthly vs twice monthly rev share changes, apples to apples same periods, net same amount of days.

I want to be convinced but have not seen the data and calcs to back up the argument. Ham’s data, while I appreciate the effort, does not show this.

If you pull the daily eUSD TVL, and eUSD TVL per wallet into a CSV, I am happy to work with you to create this apples to apples comparison.

As previously mentioned, I support eUSD rev share to fintechs. I do not support the current frequency of changes without more detailed rationales from recipients. I remain concerned about eUSD governor fatigue and decreasing overcollateralization without seeing a quantified benefit.

Thank you for championing eUSD for all the stakeholders.

eUSD daily TVL from Feb 1 to Aug 1, 2025 (the inclusion of Aug 1 is intentional here for analysis flexibility later on)

Ugly Cash wallets – daily eUSD TVL from Feb 1 to Aug 1, 2025

Sentz wallets – daily eUSD TVL from Feb 1 to Aug 1, 2025

If daily data is unavailable, use 1st and 16th of each month for a consistent baseline, enabling clean comparisons of bi-weekly, monthly, and quarterly revenue-share models.

This approach ensures a larger, consistent dataset instead of cherry picking a few months of irregular calendar UC/Sentz actuals.

Run the analysis in two formats:

Period-ending TVL balances

Average TVL balances for each period

Hypothesis: Monthly frequency will sufficiently incentivize participants, reduce admin load, enable richer community dialogue on whats moving the needle, and limit governor fatigue. If quarterly results show similar alignment, it should remain on the table.

Regardless of immediate decision outcome, this analysis will strengthen eUSD decisioning for years to come.

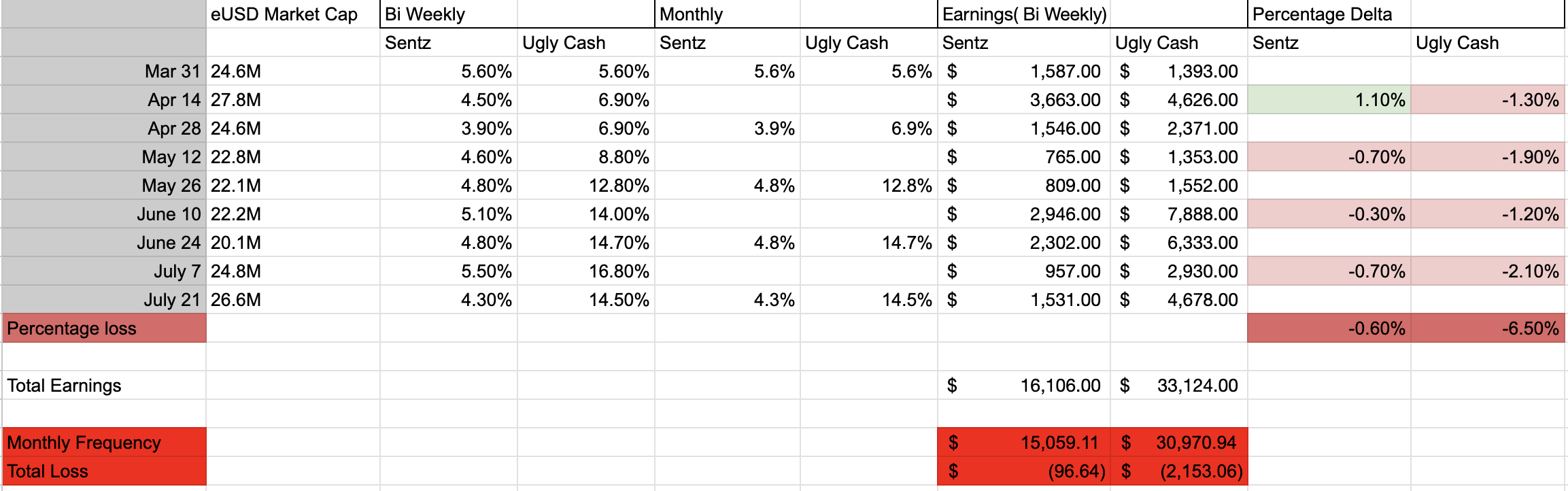

Your hypothesis is incorrect, according to my calculations, UC would sustain about 6.5% of losses with keeping to a monthly frequency, this roughly comes out to about $2,153 from Apr 1 to August 1st. Data is not reliable enough from February 1st to April 1st, this is because there was a sustained period where auctions didn’t run as well as the Rev Share percentages stayed about the same during this time. Bi weekly data was selected as it lines up better with when the percentages change from the RevShare updates.

There are a few takeaways of my own going through this data.

Initially just doing napkin math in my head, I had though that Sentz would not be impacted by switching to monthly, as they were not experiencing the same growth as UC. This was incorrect as they are indeed negatively impacted.

Auctions need to be more consistent, the income is extremely variable that the FinTechs are receiving.

Switching to monthly would inflict compound losses on the Fintechs, and my analysis is that this is bad.

How can we improve from an optimistic governance standpoint, and what can be automated so that we can continue to support our FinTechs?

The next RevShare update will be on the forums tomorrow and I hope to have your support.

I remain a strong supporter of the eUSD rev share for fintechs and was among its earliest champions at Reserve (modeled after 1970s Visa co-op). What I do not support is the current high-frequency cadence (24x/yr run rate) of eUSD rev share changes that creates governance fatigue and leaves the community without clear updates on what’s working or not. Others have expressed the ongoing decay of RSR overcollateralization and yield to stakers as a concern, however this is not my concern.

Referring to Tom’s post above: Twice-monthly, monthly, and quarterly results will never match, and we shouldn’t expect them to. What matters is agreeing on a “materiality threshold” that signals when the difference is meaningful enough to justify changes. Is that threshold 5%, 10%, or another figure? The real analysis isn’t just the percentage, it’s what we get in return (for example Ugly Cash strategy and results disclosures, vs not). For example, cutting governor workload by 50% and refocus attention on higher-priority matters if it costs only a 6.5% inefficiency in revenue sharing.

I have taken Tom’s table and built it out in this sheet for you to inspect formulas, check math and for us to get the correct inputs.

Two changes are necessary:

Update column F with correct inputs (Tom I can make you a co editor on the sheet if you’d like to add)

Either complete March data, or completely remove it (currently, it overcounts in favor of monthly!)

As you can see in the math unless I’ve made a mistake, Monthly cadence captures the full growth of supply and yield across the period, whereas bi-weekly cadence splits it and undercounts the portion that existed after the first calculation.

A fast growing player like Ugly Cash appears makes more money on a monthly eUSD rev share change cadence, at 50% less work for eUSD Champion and Governors.

This is time better spent on growth, comms and safety. For example the Fintech rev share could have a public comms reply-guy strategy for similar size apps in the UC and Sentz peer set so they too can enjoy the fruits of eUSD.

Once the above issues are resolved, we should run the analysis against the quarterly cadence in two formats: (a) using period-ending TVL balances and (b) using average TVL balances per period. This will give us a formula that ensures fairness for both fintechs and stakers.

Thank you for reviewing the work. There may be errors in the spreadsheet, and I appreciate everyone’s attention to detail.

As stated a few weeks ago, I will be voting AGAINST any further eUSD rev share changes until this analysis is complete. I remain hopeful that revenue participants Sentz and Ugly Cash will commit to a reasonable cadence of updates for the Reserve community on what’s working, what’s not, and where support is needed. After all, it takes a village.