Good catch James, Sentz should be at 4.4, however the Revenue stands.

As mentioned in my previous comment, from Feb 1 to April 1 the data is not reliable. No auctions were ran during the month of March. Additionally, in March one of the RevShare updates didn’t pass and by default stayed at a monthly cadence for that month.

Here is the tx for the Revenue auction: Ethereum Transaction Hash: 0xecc9b06daa... | Etherscan

”Missing the eUSD overall yield for each period that gets split amongst sharing parties” The revenue that has been auctioned is a function of the yield and is left out as it is not a data point that helped me come to the conclusion that I did.

“Also if you can share a read-only of your data table that could accelerate my analysis..” I dont want this doc to be shared right now, Ham and I both calculated two different ways and came up with two different results. We both came to the same conclusion that a monthly cadence will create compounding losses for the FinTechs. I’d like to see your own analysis to prove us both right or both wrong.

”creates governance fatigue” I dont think there is any evidence to support the claim of governance fatigue.

”6.5% loss is probably immaterial…” I strongly disagree, the FinTechs can easily go to T-bills or sUSDS and receive 100% of the yield of their customers funds. I am not in favor of intentionally inflicting compounding losses on the FinTechs.

Ok will remove all the March data to keep it clean. So we will be using the 4 month dataset.

The math I shared, in the open, inspectable spreadsheet, shows UC making more money on a monthly cadence. It might not be correct. If you have any better inputs (all the blue numbers) to share, please do and I will modify. Or if you see anything wrong with the formulas, please say so.

@Sawyer I’d like to use your inspectable spreadsheet to clarify the formulaic math on unresolved questions, or you can fork the one I’ve constructed here (adding correct inputs) to help resolve open issues.

Two different analyses produced errors, which makes us uneasy. Ham’s work compared mismatched time periods, while Sawyer’s included at least one incorrect input. I do not have the correct inputs on how the maths were calculated (so i cannot do it myself), you do.

Mistakes happen, and that’s fine—especially when the math is transparent, inspectable, and open to collective collaboration.

Relying on ‘napkin math’ and screenshots, as mentioned above, creates unecessary risk to the eUSD ecosystem. We need to move past that by openly sharing spreadsheets in a way the community can inspect and verify.

As stated earlier, I am voting AGAINST any further revenue share changes until there is greater clarity on the outstanding questions.

Voting AGAINST the updates @Sawyer is producing signals that the voter is against the new parameters first and foremost. If I read your posts correctly, and please feel free to push back here, you want to change the cadence and introduce new reporting requirements.

To do so, the best way would be to submit an RFC, that basically copies the original RevShare RFC (which you support) but add clarification on cadence and reporting duties.

OR to abstain from voting as this reduces the overall legitimacy of the polls (less turnout), signals governance fatigue, and reduces the chances of these polls meeting quorum and passing.

Of course you’re more than welcome to vote AGAINST to express your direct opposition to the ongoing process, especially since it is coupled with excellent communication of your rationale here on the forum. This reply is meant to help to think through the options here.

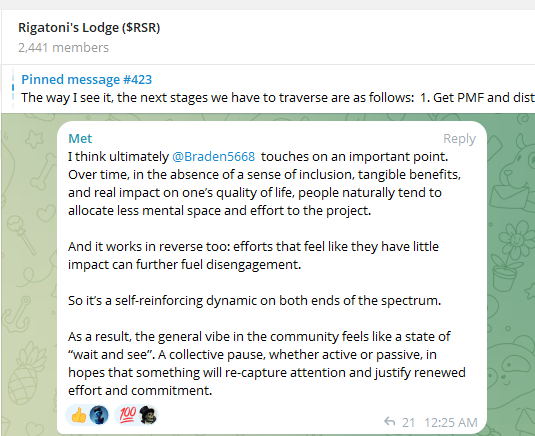

As reported at the top of this RFC, there have been 17 eUSD rev share changes in about 12 months, and tracking toward a standard cadence of 26/yr (bi weekly). The most material impact aside from the extra governance work, has been a decrease in yield shared with RSR stakers providing governance and overcollateralization.

In the most recent eUSD Quarterly report, less work is being done on awareness and brand (# of posts), and less impact is being had (impressions and engagement rate).

“The internet is no longer deterministic. It’s algorithm-driven, and not even among your own followers. Your posts are constantly being shown to a panel of users. If they like it, the panel is expanded. If they don’t, you don’t get reach. That means putting out a high volume of posts isn’t noise / spam / “low signal.” Volume is necessary so the algorithm can pick up your winners and make them viral. You have to experiment with high volume, learn quickly, and double down on your winning formats. The cost of failure is ~0. The tree falls in the forest and no one sees it. But the cost of not experimenting is astronomical.”

Additionally the quarterly reports lack any substantive updates from rev share recipients Sentz and Ugly Cash. Are we in this together, or not? What’s working for them, what’s not, and where can the community contribute?

TLDR

Heavy focus on revenue-share maintenance.

But…eUSD TVL is shrinking while the stablecoin market expands.

Little eUSD brand awareness growth; we’re absent from conversations with potential Fintech app partners.

Excessive governance churn is creating fatigue, lowering safety through divided attention, meanwhile actually reducing eUSD overcollateralization.

No feedback loop from Fintech partners on what’s working and what’s not.

What’s been repeatedly suggested, yet punted, is rebalancing eUSD’s governace and growth cost/benefit equation. The hypothesis: shift effort from governance churn toward brand-building and awareness, which would better serve the ecosystem.

To move forward, we need an apples-to-apples comparison in a transparent spreadsheet with inspectable formulas, showing how 26x/year, 12x/year, and 4x/year revenue-share adjustments impact stakeholder payouts. The goal is to identify the threshold of diminishing returns and weigh the overall cost/benefit for the eUSD community.

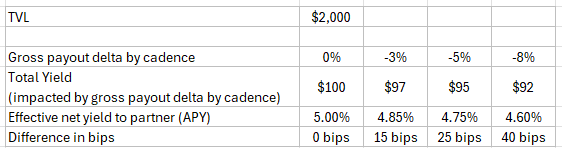

“Gross payout delta by cadence.” If governance lift is reduced by more than 50%, is a 3% payout delta material? what about 5% or 8% delta? What is the delta target we are optimizing for and why?

“Effective net yield to partner” (APY). How does gross payout delta by cadence translate into effective net yield to partner (APY)?

But we can’t evaluate this in isolation. We also need to track the net yield actually paid to Sentz and Ugly Cash on their eUSD holdings. How does it stack up against alternatives like USDS or GHO? Quantitatively, what should eUSD’s yield premium be over sUSDS or competitors—50 bps, 100 bps, 200 bps?

IMO we should be voting AGAINST these revenue-share change proposals (or not putting them up at all) until a thorough impact analysis is completed (correct, transparent formulas, shared) and there is community consensus understanding, not punted. This situation perfectly illustrates eUSD’s current challenge: busywork theater, not enough impactful work.

We should complete this analysis and revisit the TLDR above to see what can be rebalanced for the overall good of the eUSD ecosystem. It won’t be perfect, but it can be much better.

I don’t mind putting up new proposals however I am hoping the current, compensated eUSD RToken Champion will take the lead on information and analysis disclosures and pulling the eUSD community together. Lot of opportunity here to compound the current eUSD RToken Champion configuration.

The comments here on the eUSD Q2 report further illustrate the opportunity.

We want eUSD to win. We want the RToken Champion to win. We want our fintech revenue-share partners to win. We want stRSR governors and overcollateral providers to win.

Hey James, I’d like to illustrate more clearly why it is important to continue these bi-weekly RevShare updates for the FinTechs.

In this example we will have two scenarios. Scenario A and scenario B. In Scenario A we will run the auctions bi-weekly. In scenario B we will run the auctions monthly.

I’ve highlighted in bold Week 3 Scenario B. If we keep the RevShare updates monthly, week 3 is where the FinTech, that is growing, will loose money. By not proposing that second update for the month, the FinTech that is growing will continue receiving revenue at 5%, even though their holdings reflect they should be at 10%.

Jan 1 2025, Ugly Cash’s RevShare percent was at 3.66%, and now, it currently sits at 17.39%. By keeping with the bi-weekly updates we have minimized any losses to Ugly Cash.

You’ve pointed out my incorrect data point as it pertains to Sentz, and so I understand wanting to discredit the entire Data set. In this case, I’d point to Ham’s data. Ham articulated how much loss the FinTechs would experience in both quarterly and monthly scenarios. Is Ham’s data not sufficient?

In my opinion, it does not matter how small the loss is, I do not want any current(or new) FinTech to experience any loss in the RevShare program.

Lastly, you’ve mentioned governance fatigue as one of the main reasons for moving the bi-weekly RevShare updates to a monthly cadence. Can you specify what data has led you to this conclusion?

In my opinion, it is pretty clear that we are seeing a renewed strength in eUSD governance and I very much want this to continue.

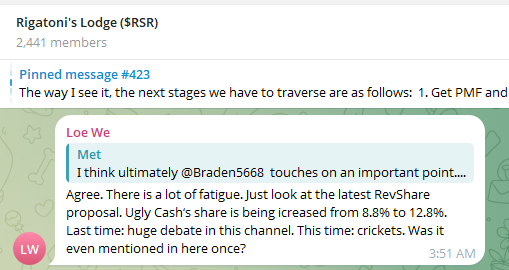

Examples of the renewed strength(opposite of fatigue) that I see, are the new comments in the eUSD quarterly report alongside this excellent conversation that we are having as a community.

There are 389 voting addresses on eUSD, yet only about 4 or 5 voting, mostly direct delegates from core team. This is 389 different talents and competencies that might potentially contribute, if asked, and if they felt their voice mattered.

Here is what it was a year ago, here it is today. TLDR: decreasing # of voices. Not the direction we aspire for, unless decentralization in the Reserve ecosystem has been deprioritized.

Not to mention I get private DMs from the community unsolicited almost monthly on this. Its just become easier for people to bail out.

BIGGER ISSUE

The bigger issue is how eUSD brand building is progressing, since it was central to your original RToken Champion 3% revenue participation proposal.

eUSD TVL is trending down, and your own report shows awareness and outreach declining against the backdrop of a stablecoin boom. The strategy of securing fintech rev-share partners is strong, but it depends first on marketing visibility, and later BD outreach to close. Hundreds of new fintech apps and stablecoins launched in the past year, many of which might benefit from a two-year-old, battle-tested eUSD that already pays. The lowest-cost way to get into their initial consideration is probably something eye-catching on X, Reddit, or YouTube.

Leadership and direction are needed, though no one expects you to carry this alone. Doubling or tripling eUSD awareness would be meaningful even if no fintechs join the rev-share, and it would strengthen RSR and the wider Reserve ecosystem.

There are 389 voting addresses on eUSD with skin in the game, many ready to help if asked and included. A simple invitation could turn them into amplifiers of the eUSD value proposition. We’re hoping you’ll step forward, set the tone, and rally the group, while keeping your revenue participation intact and broadening the effort.

I imagine you too have finite time and cutting back governance administration to focus on eUSD awareness and growth measures are just one unnovel suggestion on how to do it.

As just one of the eUSD stakers, I’d gladly support more than 3% for the RToken Champion—if results justify it, and that accountability should cut both ways.

eUSD brand building has slowed. Shows no signs of increasing awareness with a 3rd (or 4th) fintech for the rev share opportunity.

eUSD TVL has declined.

eUSD safety has weakened, both in community attention fatigued by repetitive activities and overcollateralization.

Governance diversity has not improved and in fact has eroded some compared to a year ago, raising both safety and centralization concerns. The current concentration of voters creates a “why bother” attitude in the community, as you’ll see scanning the Forums (Mallo’s post last week) and the Lodge.

The eUSD rev-share frequency debate highlights just a ~0.15% yield payout difference* for UglyCash holders, a trivial gain weighed against the three larger issues above. Adding additional context: RSR holders provide the liquidity cushion to sell RSR and fund the operations of UglyCash and its predecessor for the last five years. The eUSD yields are market leading to UglyCash, with no staking required by eUSD.

*I’ll share transparent, inspectable maths later this week.

gm, have enjoyed following the discussion here and over on the Q2 Report post but am starting to feel that the conversation is fragmented between these two posts and moving away from actionable next steps to re-align governors and fintechs.

So far the discussion has been around reducing the frequency of the Rev Share updates and the maths around this before moving into what this time could be used for instead, brand building. Which while being a excellent conversation has deviated outside of the Fintech Revenue Share Programme. As governors we can’t dictate the time that Sawyer allocates to eUSD nor should we think we can, we can only look at his outputs, weigh-up if he has consistently added value and if we should continue sharing revenue with him. Although i’m sure these suggestions and ideas go a long way to help him decide where his time is most valuable like they do with me and the ETH based RTokens.

While brand building is important I think we should nail the programme itself before we start wheeling it out in front of other fintechs and asking them to participate. In my last post I outlined 3 areas of the fintech revenue share programme that should be improved; fintech transparency, the frequency of the fintech rev share ratification votes and dropping over-collateralisation.

Revenue Share Update frequency

With regards to the Revenue Share Update frequency I’m actually in favour of the current structure to continue and feel further data collection and modelling is redundant. I’m sure Sawyer is fairly proficient in these now and makes a good point that more fintechs will only join this programme providing we have a sure and solid way to accurately track their balances, which atm we don’t. I’d rather use time to explore ways to more accurately track fintech balances and reduce the amount of ratification votes. I know @mattimost commented that optimistic governance will likely come in Q4 and @0xJMG idea of reducing the frequency will solve the latter but doesn’t more accurately track fintech balances. Maybe something more akin to the per block method @Raphael_Anode discussed in the last GovOps is a more elegant solution addressing both concerns at once.

@Sawyer What are your thoughts here? Have you or are you planning to explore changes to the programme to track fintech balances more accurately and reduce vote burden or do you plan to continue under the same mandate until optimistic governance comes in Q4?

Lack of Transparency / Dropping OC ratio

I haven’t seen any further conversation on these points. Granted a lot of these conversations have likely to have been had in DM’s they eventually needs to come full circle updating the community on progress or lack thereof.

@Sawyer have you made any progress addressing these concerns? What is the current stance by fintechs on these matters? Are they planning on coming back to the forums to address them in due course? Paging @josh for visibility also.

As promised, here’s the cadence issue sliced and diced—at least one surprise in there.

One part you raised @ham deserves more spotlight: “While brand building is important, I think we should nail the programme itself before wheeling it out in front of other fintechs and asking them to participate.”

I’d further this with brand building is a subset of the strategy programme.

Normal flow: agree on strategy, map GTM comms/BD plan, run it, adjust. Partner meetings come in the later parts.

The eUSD fintech rev-share idea is exciting, but the plan and components need clarity. How do we persuade the market of the merits? What support is required from CC or ABC Labs? What can be mobilized from the 390 eUSD stakers, the wider RSR community, and the two current fintech partners?

One question I’ve been thinking about is what is eUSD’s differentiated value proposition for Fintech’s?

Seamless yield on wallet balances without staking hoops?

Proven resilience through volatile markets and black swans?

Decentralized governance with automated onchain operations that reduce operating costs, are fully verifiable and shield distributors from a regulator “stablecoin issuer” classification?

Market leading stablecoin yield (potentially boosted with RSR rewards)?